A Brief Anatomy of Gold Bull Markets

It's Déjà vu all over again: Gold prices and gold stocks are up again! Many market participants who missed the gigantic move of mining stocks last year may think that the spike in mining shares this year is real and want to take advantage of this joyful bandwagon. However, this gold upward move could still be cyclical in a secular bear market. Unlike last year, most gold/silver stocks seem to hesitate to join the gold/silver parade, reflecting the investors' doubt about the stamina of this rebound, even though political or economic uncertainty looms.

For a start, let's first look at the returns of some top gold/silver stocks in 2016. Last year, from the low points to the peaks in August, most gold/silver stock prices doubled or tripled, with some jumping even more than that:

- Northern Dynasty Minerals (NAK) up 1625% from $0.20 to $3.45, now $2.90;

- First Majestic Silver (AG) soared 798% from $2.4 to $19.15, now $10.75;

- Sibanye Gold (SBGL) rose 423% from $3.95 to $20.68, now $8.86;

- Pan American Silver (PAAS) ascended 300% from $5.36 to $21.56, now $21.08;

- Royal Gold (RGLD) climbed 258% from $24.33 to $87.16, now $70.70; ...

These heavenly metal shares advanced so quickly that many investors simply missed the rally. How did this rebound happen? In retrospect, we know it just recouped some lost land due to negative over-reaction to the Federal Reserve's hawkish comments on interest rate policy. In 2016, the Fed raised the federal fund rates only once rather than three times as anticipated by many market players in the early of the year.

Now the Federal Reserve seems to being playing a similar game as last year, believing that it is proper to hike interest rates three or four times this year. But the market thinks otherwise, as federal fund rate futures imply two instance of interest rate hikes on the horizon. This may be the main catalyst to drive gold prices up 10% so far, although the fear of inflation, geopolitics or temporary softness of the US dollar may also partially contribute to the recent gold price climb.

Two Secular Gold Bull Markets

Unlike other commodities, whose prices are determined by supply and demand, Gold is a political metal. Its price can fluctuate due to factors like geopolitics, inflation/deflation, currency movements, monetary policy, and supply and demand. During the past 50 years, gold/silver prices experienced two secular bull markets (Chart 1 and Chart 2):

1. The Gold Bull Market From 1971 To 1980

On August 15, 1971, President Richard Nixon astonished the world by abandoning the Bretton Wood Agreement, which fixed the US dollar to gold and the rest of the world's currencies to the dollar. This Nixon shock devalued the US dollar, thereafter letting it freely float against gold and other currencies, and officially terminated the gold standard.

From the gold low price of $38 a troy ounce in August 1971 to $672 a troy ounce on September 8, 1980, the price of gold rose 1668%. In this gold bull market, the price of gold had two major upward movements driven by geopolitics, inflation, and monetary policy.

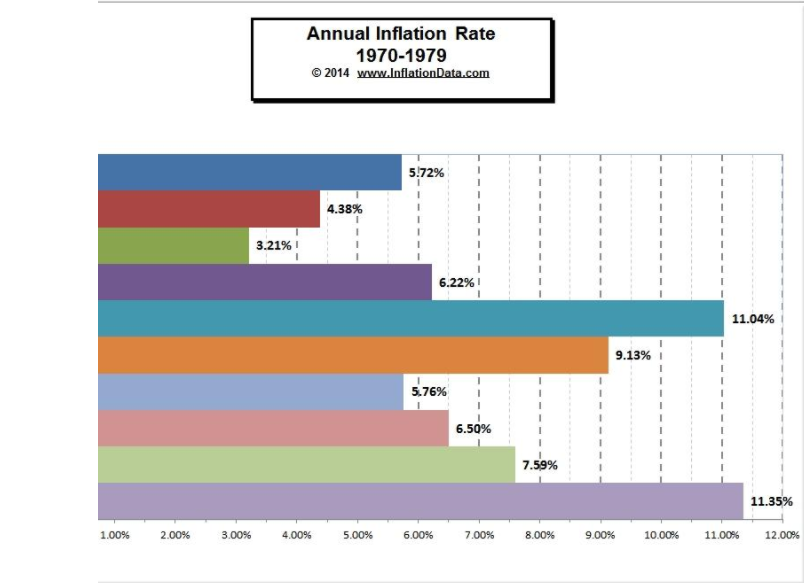

- From the bottom price $38 in 1971 to the peak $195 on December 30, 1974, the price of gold climbed 410%, then fell back to $113 on August 10, 1976, dropping 42%. This gold bull resulted primarily from President Nixon's twice devaluations of US dollar and Arab oil embargo, which sent the price of oil from $2.95/barrel to $11.65/barrel, leading to towering inflation in the mid-1970s. The average annual inflation rate during this period was 6.2%, from a low of 3.22% in 1972 to a high of 11.04% in 1974 (see chart 3). After an Arab oil embargo, the pace of inflation accelerated from 6.22% in 1973 to 11.04% in 1974, and so did the price of gold.

- From the lowest price of $113 on August 10, 1976, after a slumber for nearly two years, gold prices advanced again to $672 on September 8, 1980, rising 494%. The major events in this period included the Iranian revolution and Iran-Iraq war. After the Iranian revolution in 1979 and Iran-Iraq War in 1980, oil production in Iran almost stopped and Iraq's oil production also declined dramatically. This oil crisis caused oil prices to more-than double to $39.5 a barrel in one year. The average inflation for six years was 9%, far higher than the long-term average 3.2%. The advance in gold price corresponded to the skyrocketing inflation rate: 5.76% in 1976; 6.5% in 1977;7.59% in 1978; 11.35% in 1979; and 13.5% in 1980 (See charts 3 and 4).

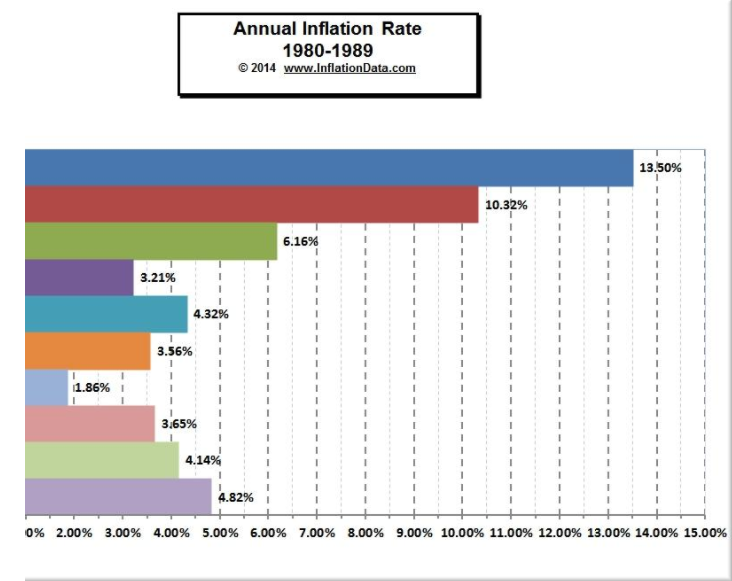

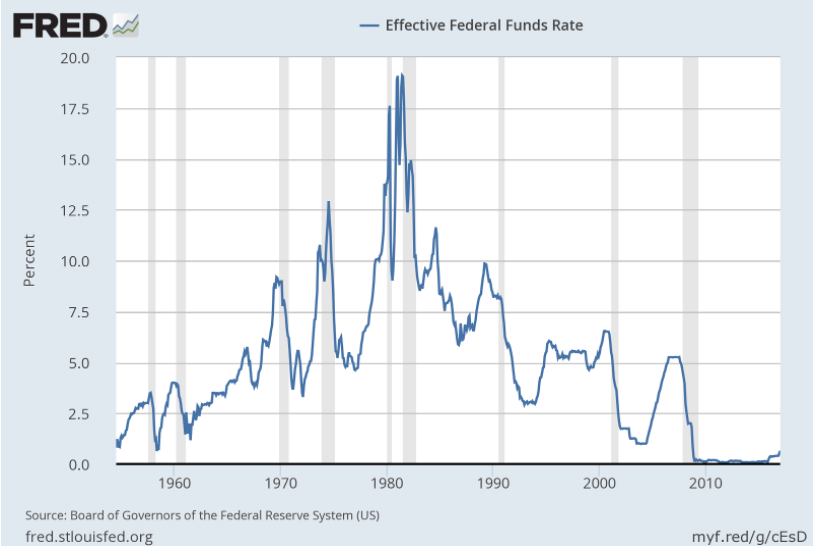

To fight hyperinflation, Paul Volcker, then-chairman of the Federal Reserve, boldly raised interest rates to 19.1% in 1981 from 4.68% in 1977. The federal fund rates moved in tandem with inflation rates (see chart 5). Mr. Volcker's courage saved the economy in the face of near unanimous denunciation and derision.

2. The Gold Bull Market From 2001 To 2011

After twenty years of doldrums, gold began to rally in late 2001. A stock market multi-year low, the 9-11 terror attack, and the Iraq War became the vital events for this fledgling gold price rise. From a low of $272 in November 2001 to $1806 in September 2011, the price of gold advanced 560%.

Interestingly, this gold bull also ran two major stages. (1). From a low of $272 in November 2001 to $959 in July 2008, gold prices moved up 252%, then retreated 25% as the Global Financial Crisis worsened in latter 2008 (See Chart 1). Dramatic demand for gold by hedge funds surfaced in 2001 as the US would run a record trade and budget deficit. China's overall industrialization took off in 2002, providing the pivotal catalyst for the super bulls in metal and oil prices.

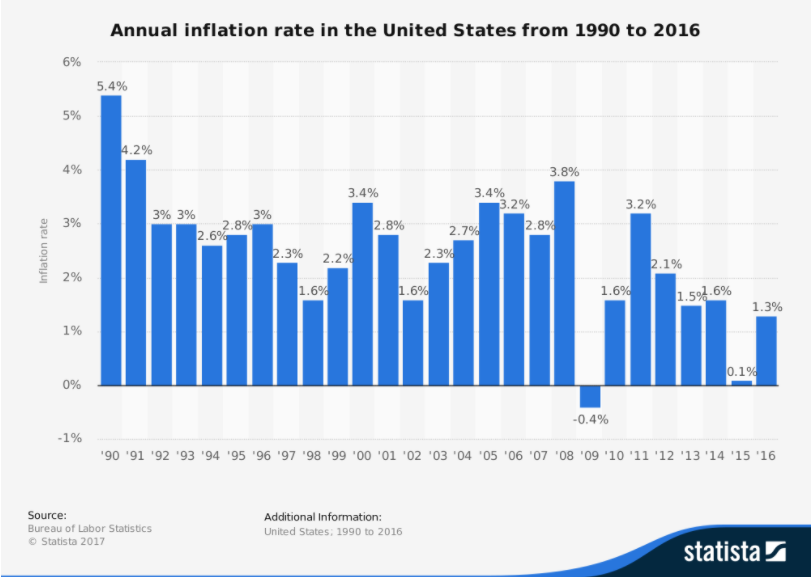

During this period, the inflation rate slowly budged up from 1.6% in 2002 to 3.8% in 2008, while interest rates kept moving down from 6% in 2001 to 1% in May 2004, then sped up to 5.25% in August 2006 as the Federal Reserve looked likely to be behind the yield curve (See Chart 6). This shows that gold prices did move in sync with the inflation rate, but randomly shifted with interest rates during this period. (2). From the low of $712 in November 2008 to $1806 in November 2011, gold prices mounted 153%.

After the financial crisis, global central banks adopted quantitative easing policy to prime the pump. By flooding the financial system with money, central bank pushed down interest rates, while encouraging inflation. Interest rates dropped to 0.1% from 5% in August 2007, and the inflation rate climbed back to 3.2% from -0.4% in 2009, then gradually drifted down afterward (See Chart 6).

Implication for Current Gold Rally

Since then, the price of gold has rebounded 10%. It is too early to tell if this 10% rally is the incipient of the third secular gold bull market. Based on twenty years of time lapse between the first and second gold bull markets, the current gold secular bear market should have further to go. Present markets are still full of gold bulls and need more time to exhaust hope for gold.

It is premature to conjecture that Trump's fiscal policy will fan the inflation flame. Like Reagan, who did not cut taxes until two years after he was inaugurated, Trump may also delay his tax cut for all sorts of reasons. Although the Reagan era did create a huge deficit, gold prices did not grow into another powerful bull leg.

Technically, during the twenty years of gold price sluggishness between two secular bull markets, there were five cyclical bull runs: (1).+ 57% (June 29, 1982 to January 18, 1983---6.5 months); (2). +44% ( June 24, 1986 to December 15,1987 ---18 months); (3).+15% ( September 21, 1989 to February 19, 1990--- 5 months); (4).+16% (March 31, 1993 to July 9 1993 --- 3.3 months); (5). +20%( August 15, 1999 to October 4, 1999--1.6 months).

The average rallied about 30% in nearly 7 months. Current gold price is engaging on the second upturn. The first rebounded 24.5% from December 4, 2015 to August 1, 2016, spanning 8 months. So the second rally can last 4 to 5 months longer or shorter with upside 8% more/less if factored into twenty years of previous gold bear market.

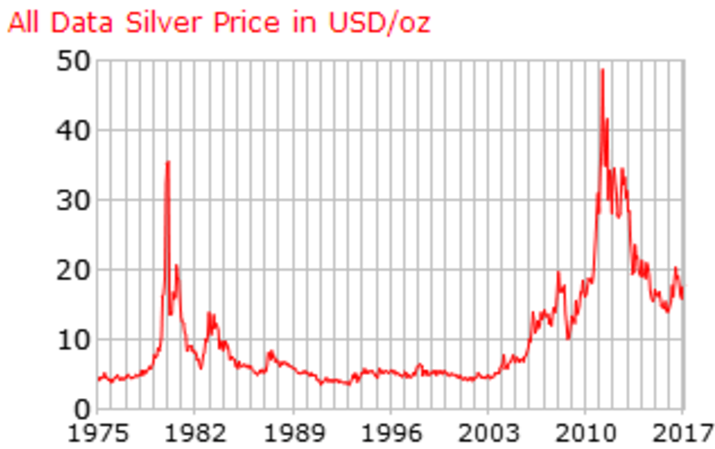

Silver bull markets could follow gold bull markets due to its similar chart pattern with gold price. If the above analysis is correct, gold/silver price could still be in the early inning of secular bear markets, and current rallies in gold/silver prices can be interpreted as cyclical rebound in long-term down trend or bottom building. The US dollar could be strengthening further in the foreseeable future, given its inverse relationship with gold prices. However, investors can still selectively participate in the cyclical gold/silver recovery.

------------------

The article was originally published on www.equities.com. I am grateful for senior editor Daniel Banas' outstanding edit. He polished the article in great detail. I also acknowledged the insight on metal sector from John Bell ---a metal specialist investor whose portfolio returned 170% in 2016. This is just a personal opinion, and personal opinion is often wrong. Currently, the author has no position on any of the above mentioned stocks, and may or may not build any position on any stocks above in the future.

Chart 1. Gold Prices From 1973 to 2017

Source: Gold Price

Chart 2. Silver Prices from 1973 to 2017

Source: Gold Price

Chart 3. Annual Inflation Rate from 1970-1979

Chart 4. Annual Inflation Rate from 1980 to 1989

Chart 5. Federal Fund Rate from 1954 to 2017

Chart 6. Annual Inflation Rate from 1990 to 2016